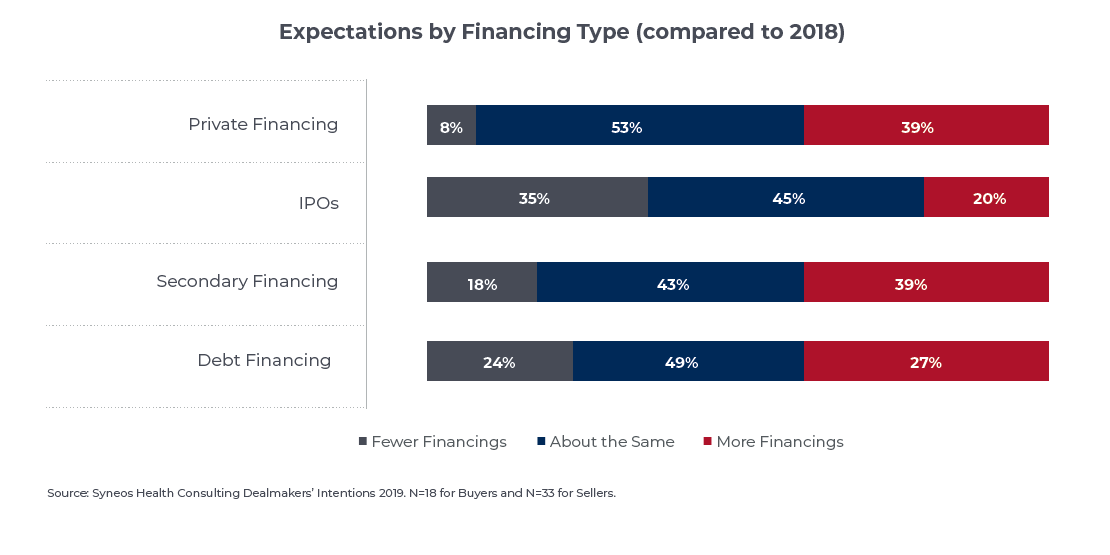

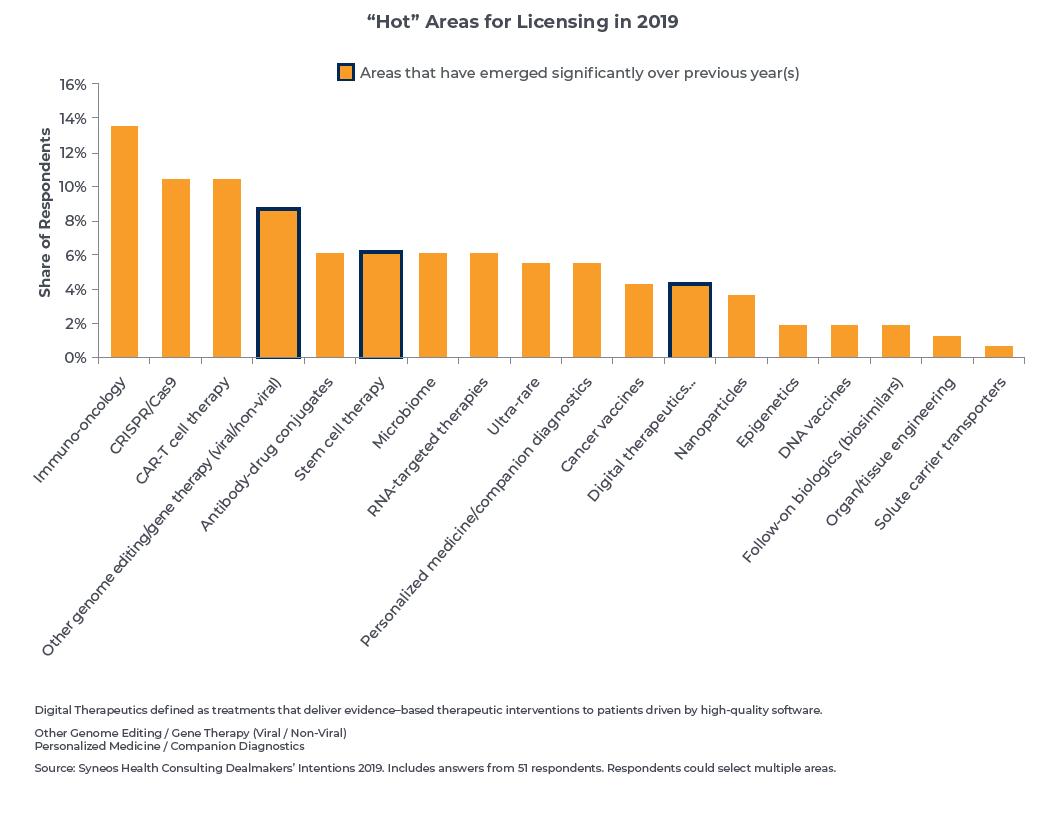

Dealmaking in the life sciences industry got off to a strong start in Q1 2019, despite a steep market decline in the last quarter of 2018 (and subsequent recovery) and a government shutdown. As a result, 2019 is on a path to be one of the strongest dealmaking years of the last decade. The private financing and IPO markets are both looking strong compared to the last 10 years, but are expected to be slightly lower than 2018. The average deal size with private financing has stepped up significantly in the last two years. Dealmaking options continue to expand for emerging companies and buyers are expressing healthy interest in early-stage assets and for the latest technologies in immuno-oncology and next-generation gene editing and stem cell therapies.

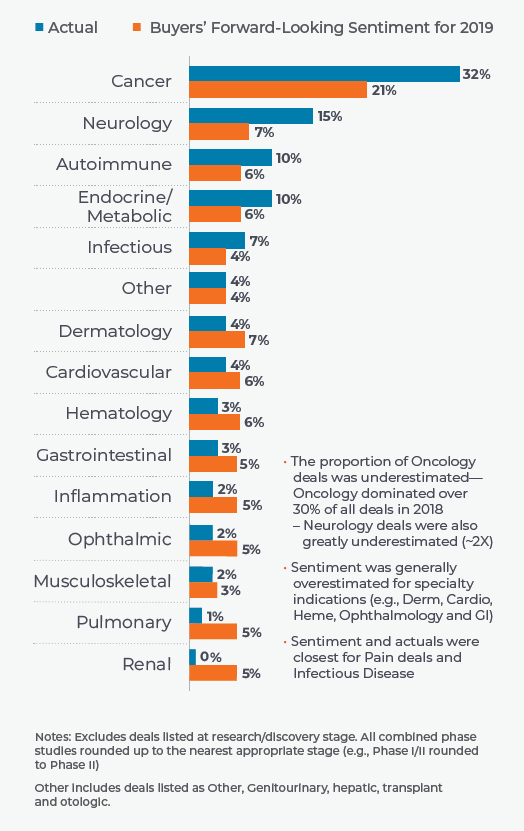

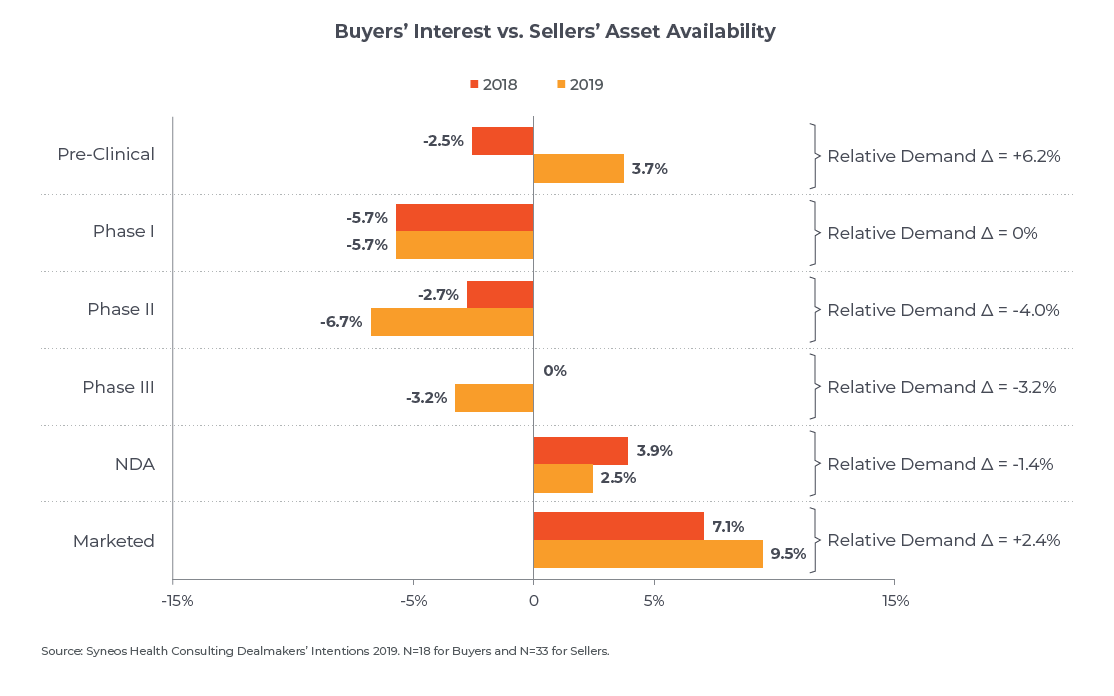

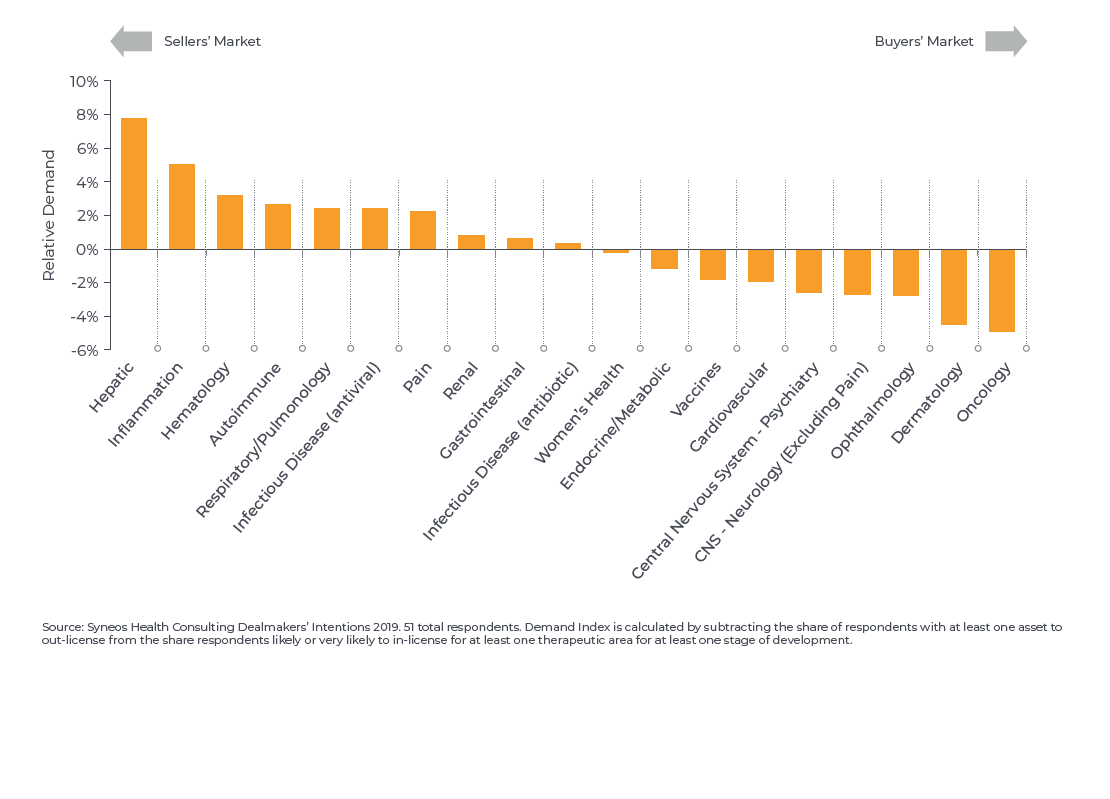

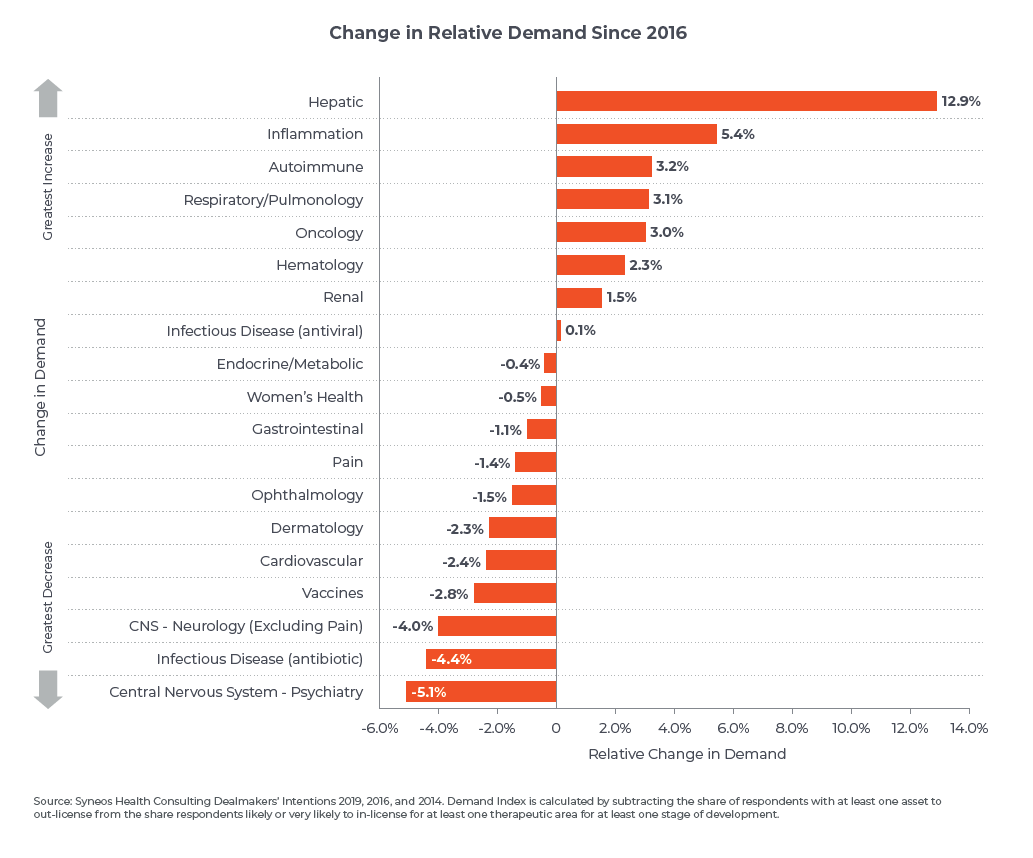

Regarding the hottest therapeutic area of them all—oncology—expectations for 2019 are that supply will continue to eclipse demand, but that prospects for dealmaking in the space remain robust. In fact, similar supply/demand dynamics for oncology were on display in 2018 and yet oncology accounted for more than 30 percent of all deals last year, exceeding buyers’ forward-looking sentiment by 11 percent. This suggests the degree to which oncology was (and appears to still be) an attractive, opportunistic market for buyers.

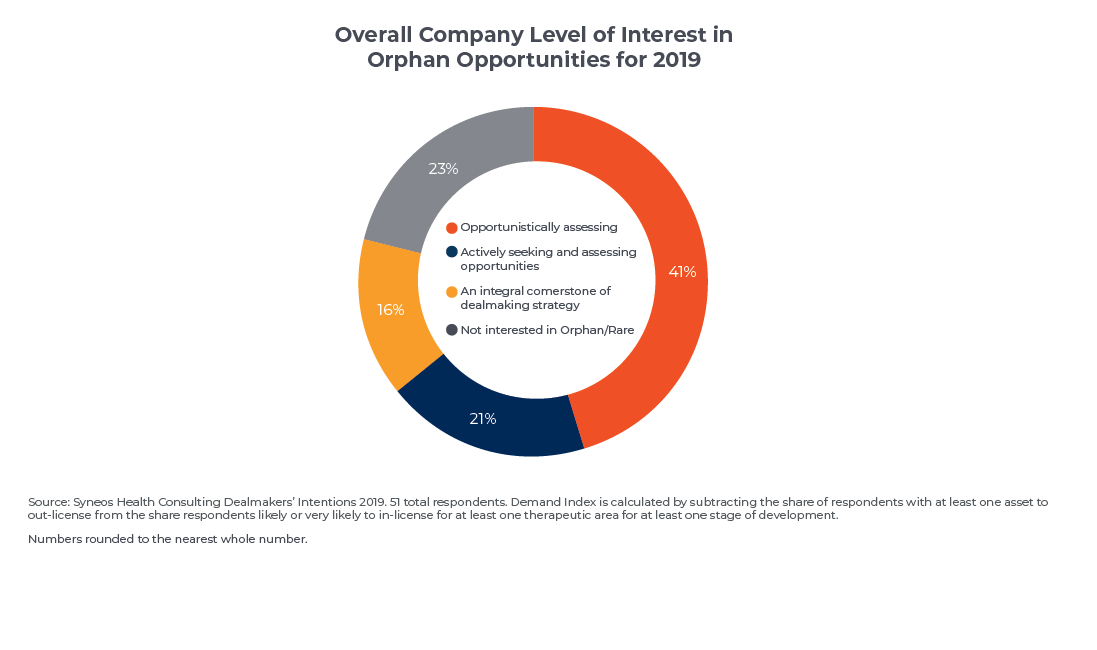

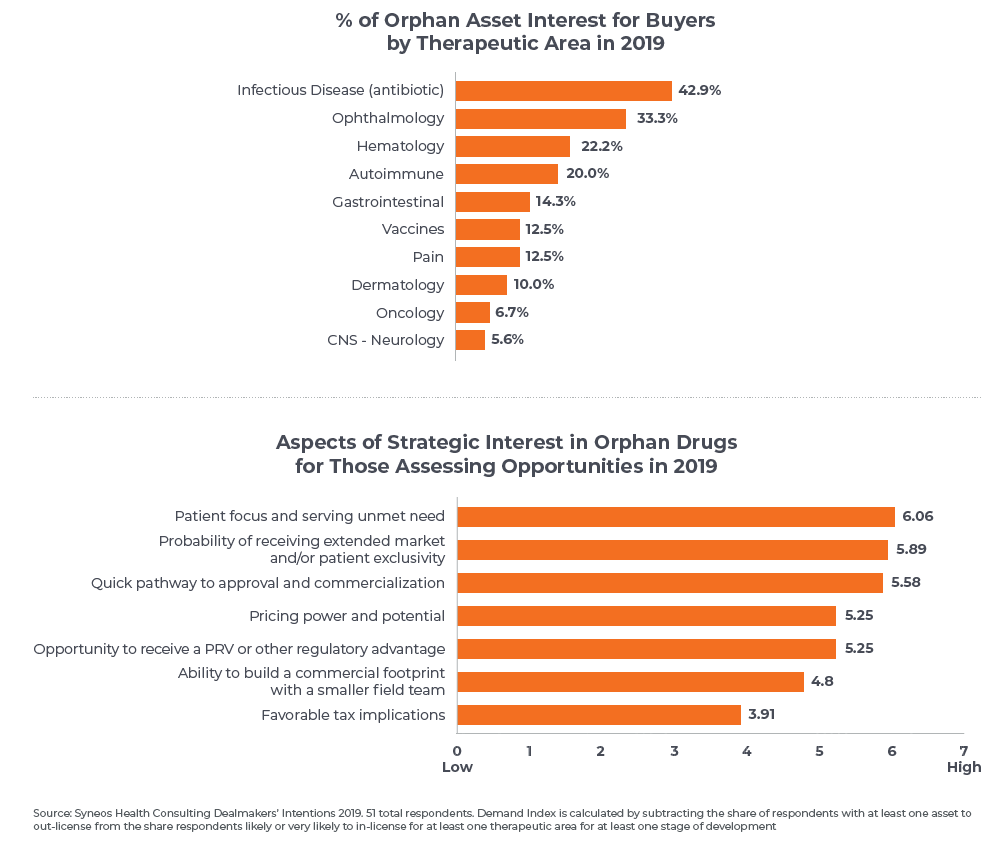

This year for the first time we assessed company interest in orphan drug opportunities, both in terms of the overall level of interest among dealmakers and by therapeutic area. Reflecting the market growth predicted for this category over the next five years, more than one-third of the dealmakers surveyed for this report view the orphan drug market as either an integral cornerstone of their dealmaking strategy or are actively seeking and assessing opportunities in the area, and another 41 percent are opportunistically assessing orphan drug opportunities.

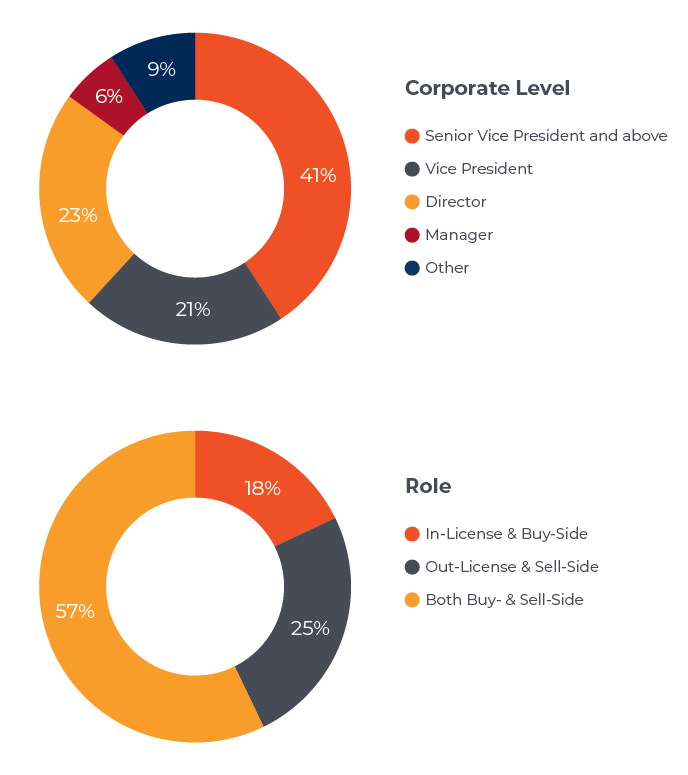

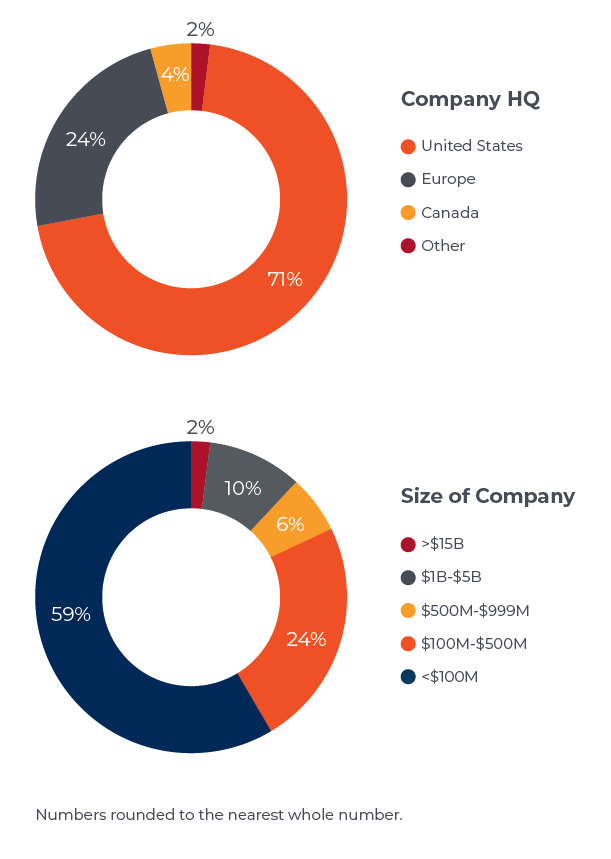

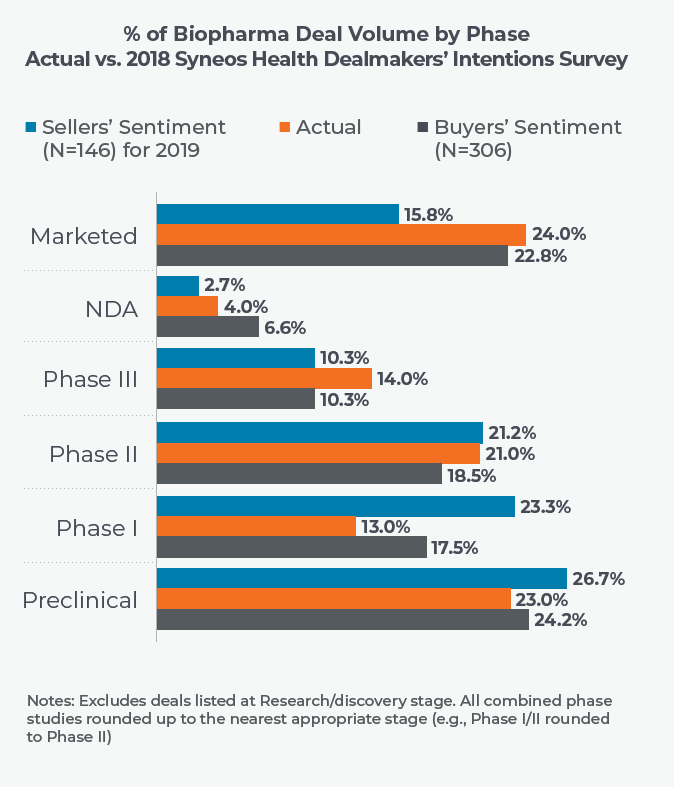

To gain more insight into what the rest of 2019 holds, Syneos Health™ Consulting surveyed dealmakers across the industry to assess their intentions for the next 12 months and put these findings into context for the year ahead. We surveyed members of the biopharmaceutical community who participate on either or both sides of deals, and who are predominantly executive-level influencers on decision-making (Fig. 1). This report, the 11th in our series, captures their expectations for deal activity, supply and demand for specific assets and different development stages, and various other factors affecting dealmaking.