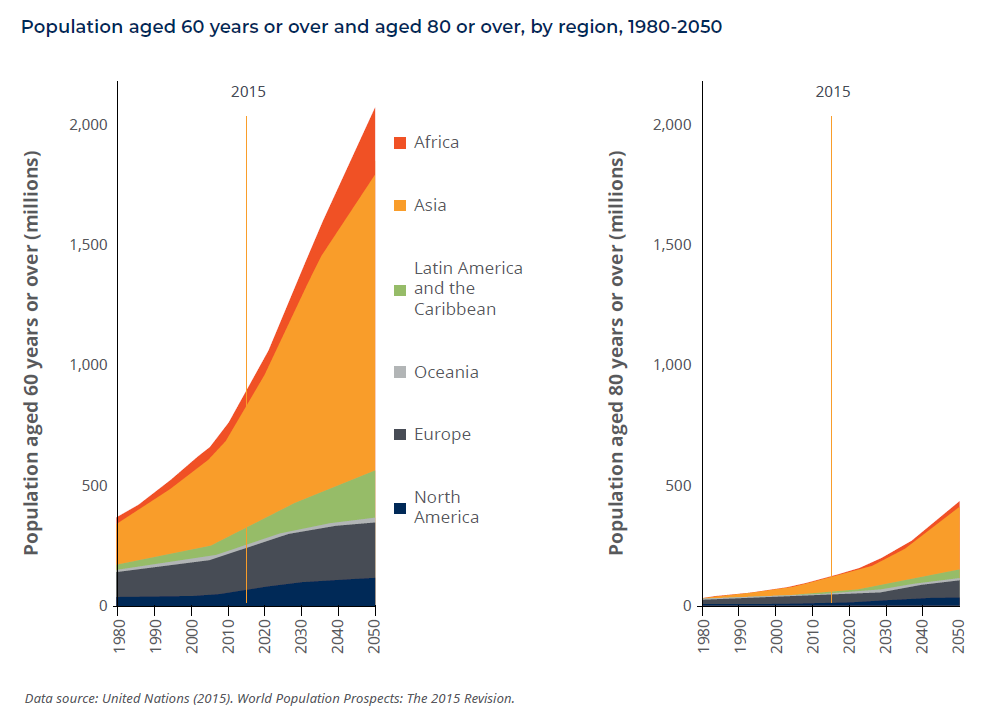

Two interrelated forces—the aging of the world’s population and the diabetes epidemic—have created an ongoing, sharp increase in the incidence of many eye diseases. In fact, the incidence of diabetic retinopathies doubled between the years 2000 and 2010.1 Vision loss is currently the leading cause of age-related disability.2

Vision loss has far-reaching social and economic repercussions beyond the devastating personal impact on the patient and caregiver. AMD Alliance International estimates that the burden of vision loss in terms of disability adjusted life years (DALYs) will reach 150 million by 2020.3

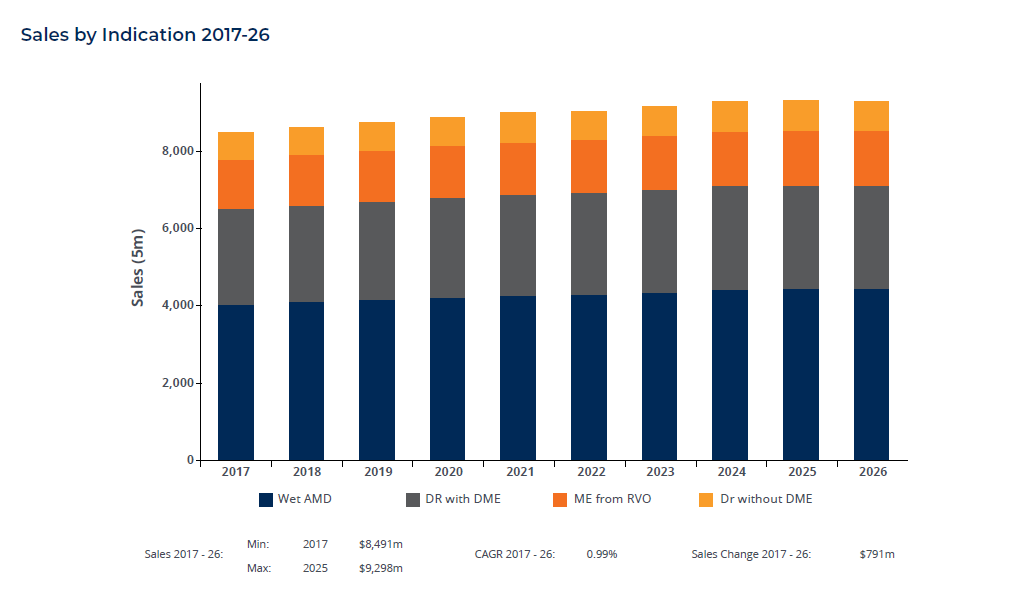

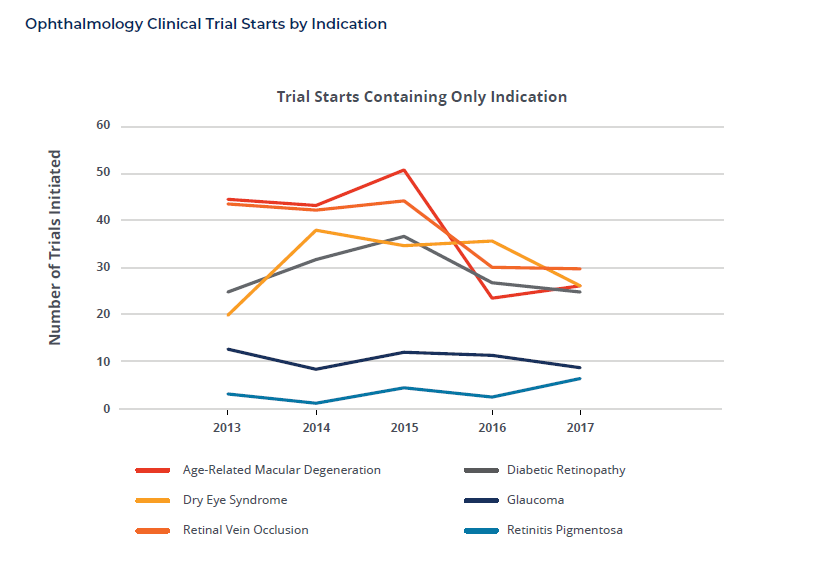

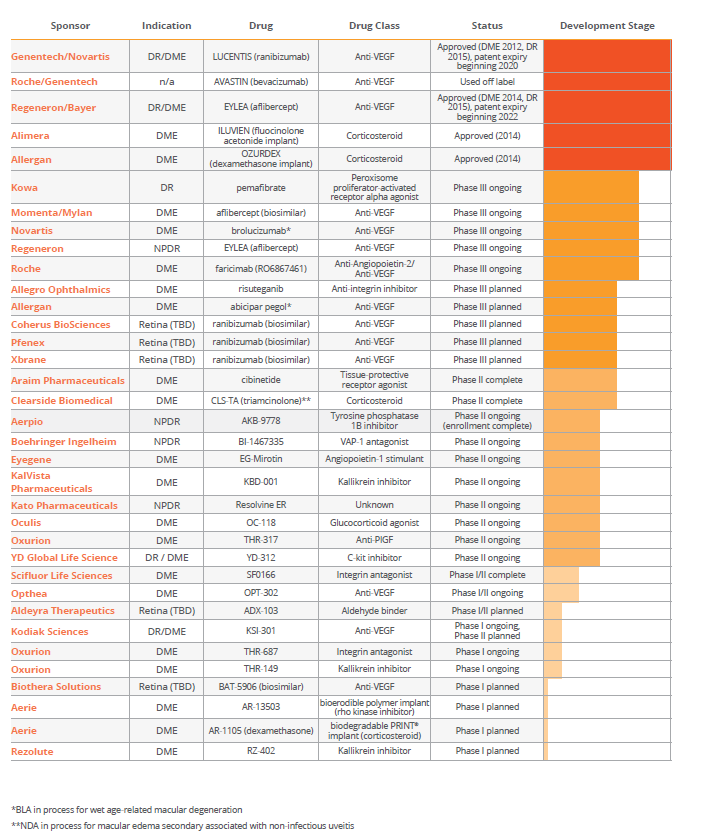

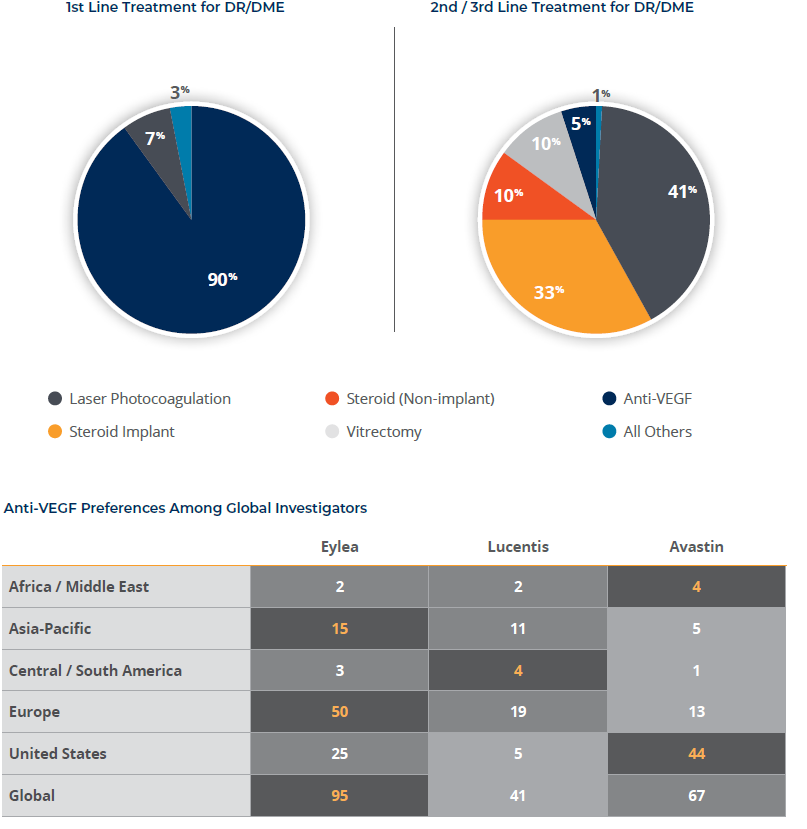

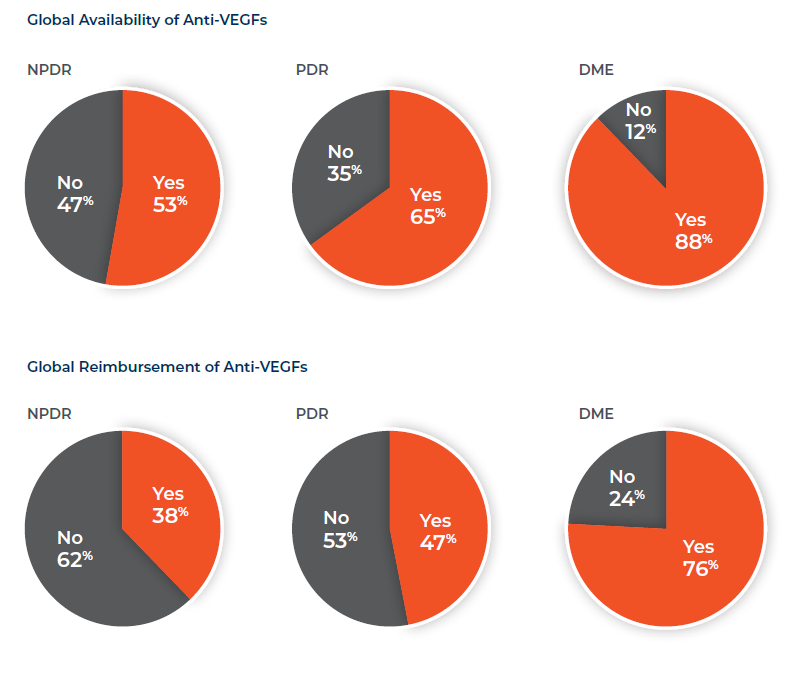

Current treatments for diabetic retinopathies are limited and focused almost exclusively on diabetic macular edema (DME). Historically, traditional therapies—vitrectomy, photocoagulation, and corticosteroids—offer no opportunity for vision improvement and come with high rates of complications. Anti-vascular endothelial growth factor (anti-VEGF) drugs have made a meaningful improvement to DME sufferers over the past decade, but even these have limited to no success in a third or more sufferers. Thus, there remains a high-unmet patient need and keen interest on the part of investigators for continued development of all treatment modalities and biochemical pathways. Fortunately, there is a robust pipeline of potential new treatments currently in Phases II and III.

Given the number of sponsors who are and will be competing for site resources and for patients to meet the needs of their developmental clinical research studies, we surveyed key ophthalmologists around the world to better understand:

- Their current therapy preferences

- The treatment pathway for patients with diabetic retinopathy (DR) generally and diabetic macular edema (DME) more specifically

- Their appetite for participating in further research

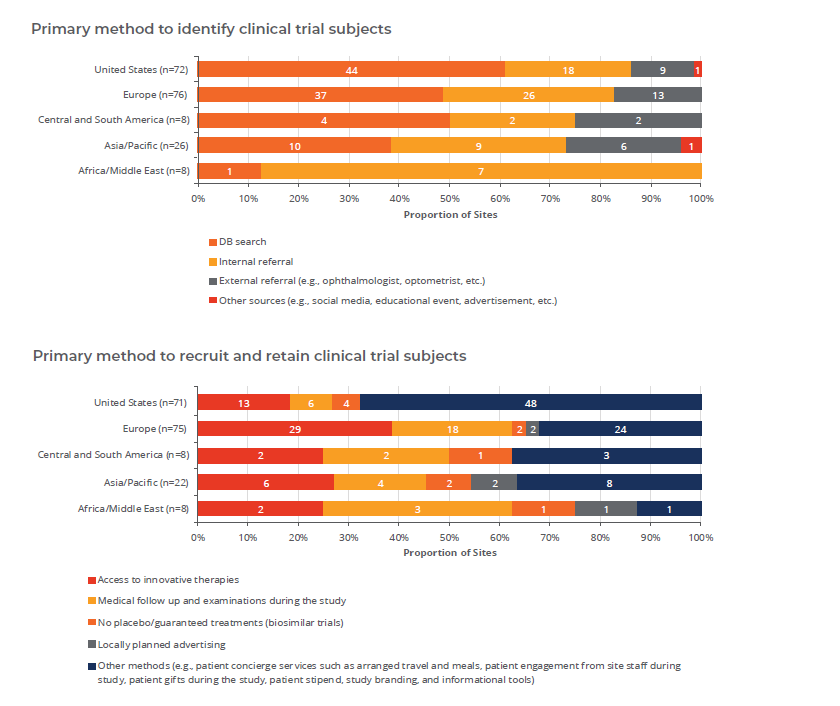

- Their ability to recruit patients

The insights from this research, presented here, are worth considering as companies conceive and advance their development plans.