Introduction

Two interrelated forces—the aging of the world’s population and the diabetes epidemic—have created an ongoing, sharp increase in the incidence of many eye diseases. In fact, the incidence of diabetic retinopathies doubled between the years 2000 and 2010.1 Vision loss is currently the leading cause of age-related disability.2

Vision loss has far-reaching social and economic repercussions beyond the devastating personal impact on the patient and caregiver. AMD Alliance International estimates that the burden of vision loss in terms of disability adjusted life years (DALYs) will reach 150 million by 2020.3

Current treatments for diabetic retinopathies are limited and focused almost exclusively on diabetic macular edema (DME). Historically, traditional therapies—vitrectomy, photocoagulation, and corticosteroids—offer no opportunity for vision improvement and come with high rates of complications. Anti-vascular endothelial growth factor (anti-VEGF) drugs have made a meaningful improvement to DME sufferers over the past decade, but even these have limited to no success in a third or more sufferers. Thus, there remains a high-unmet patient need and keen interest on the part of investigators for continued development of all treatment modalities and biochemical pathways. Fortunately, there is a robust pipeline of potential new treatments currently in Phases II and III.

Given the number of sponsors who are and will be competing for site resources and for patients to meet the needs of their developmental clinical research studies, we surveyed key ophthalmologists around the world to better understand:

- Their current therapy preferences

- The treatment pathway for patients with diabetic retinopathy (DR) generally and diabetic macular edema (DME) more specifically

- Their appetite for participating in further research

- Their ability to recruit patients

The insights from this research, presented here, are worth considering as companies conceive and advance their development plans.

The Link to Age

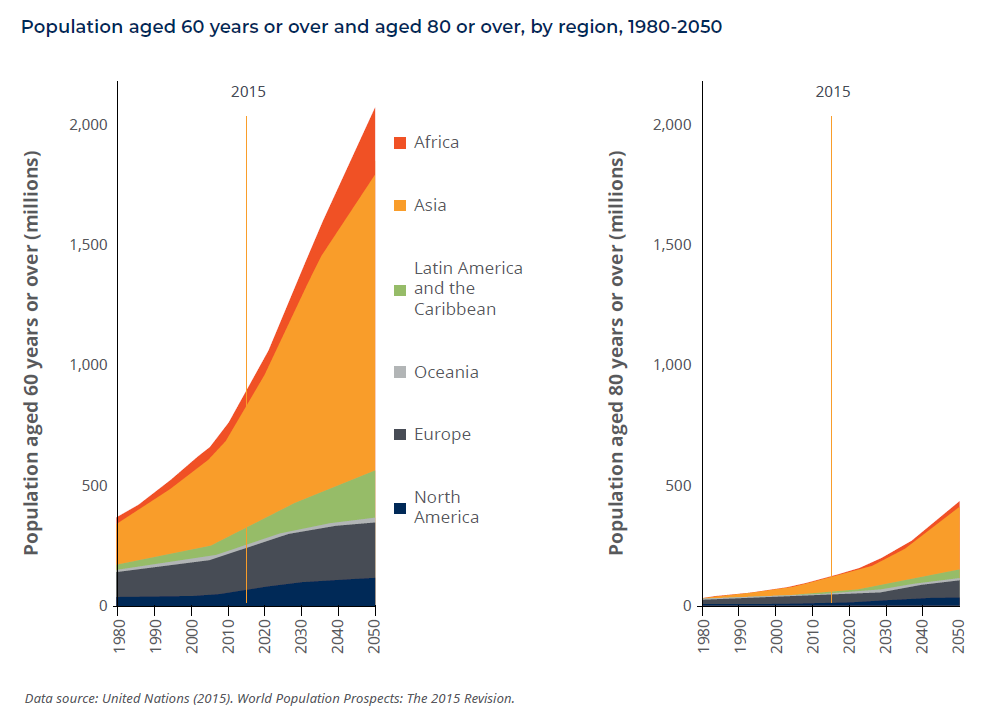

Eye diseases are highly correlated with age, so are destined to become more prevalent as people live longer. Between 2015 and 2030, the world population over age 60 will increase by 56 percent (from 900 million to 1.4 billion), and will continue to more than double over 2015-2050.4

Similarly, the incidence of diabetes also increases with age, further reinforced by an obesity epidemic, which is a primary risk factor for diabetes. This is true up until age 65, after which point growth in both the incidence and prevalence of diabetes slows.5

Headline

Glossary

- Retina: the innermost, light-sensitive layer of tissue in the back of the eye that sends images to the brain

- Macula: the center of the retina nerve tissue, responsible for image clarity, color, and central vision

- Diabetic retinopathy (DR): a disease of the retina caused by diabetes in which the blood vessels in the back of the eye are damaged

- Diabetic macular edema (DME): a form of DR. Occurs when the macula swells and extracellular fluid accumulates, causing vision loss.

- Non-proliferative diabetic retinopathy (NPDR): the early stage of diabetic eye disease. Tiny blood vessels in the back of the eye leak, making the retina swell and causing blurry vision.

- Proliferative diabetic retinopathy (PDR): the more advanced stage of diabetic eye disease that occurs when the retina starts producing new blood vessels. These can bleed, blocking vision.

- Anti-vascular endothelial growth factor (anti-VEGF) drugs: block the production of new blood vessels. Administered via injection into the eye.

Diabetes and Vision Loss: Companion Epidemics

Diabetes affects roughly 415 million people worldwide, all of whom are at risk for diabetic retinopathy (DR). About 20 percent of newly diagnosed Type 2 diabetics and about 80 percent of those who have had diabetes for 15 years also have DR.6 High blood pressure is a key risk factor for those with Type 2 diabetes in developing DR.

The prevalence of DR in patients with Type 1 diabetes is even higher, with hyperglycemia being the most consistent risk factor. Anywhere from 36.5 percent to 93.6 percent of patients in the U.S. and EU with Type 1 diabetes develop DR.7

Consequently, DR is the leading cause of vision loss in adults age 20-74 and the leading cause of avoidable blindness worldwide.8 Datamonitor Healthcare estimates that in 2016, DR accounted for 29 percent of retinal disorders in the population over age 40 in the U.S., Japan, and EU5.

Diabetic macular edema (DME) is a complication of diabetes caused by fluid accumulation in the macula, or central portion of the retina, that causes the macula to swell. The macula is filled with cells that are responsible for sharp vision used for activities like reading and driving. When the macula begins to fill with fluid, cellular activity is impaired, resulting in blurry vision. Macular edema can result from any disease that causes vessel damage in the retina; DME is specifically attributable to DR as the underlying causal disease.9

The DR/DME Market: Strong Growth with Biosimilars Looming

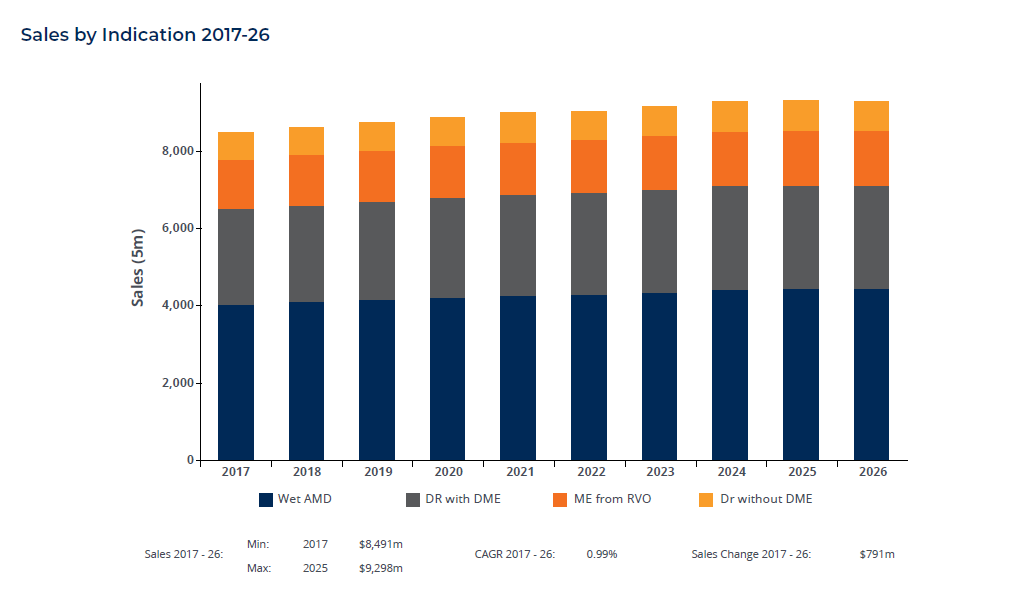

Today, the market for therapies to treat retinal diseases generates more than $8.5 billion in sales annually, and is projected to increase to nearly $10 billion by 2026.10

The market is dominated by three anti-vascular endothelial growth factor (anti-VEGF) drugs: aflibercept (Eylea™ from Regeneron and Bayer), ranibizumab (Lucentis™ from Genentech and Novartis), and bevacizumab (Avastin™ from Genentech). Bevacizumab, an oncology therapy, has never been formally approved for any eye disease, but has repeatedly been shown to be similarly efficacious and safe to its approved competitors via several randomized controlled trials (e.g., CATT, IVAN, Protocol T, CIRCLE). Avastin is used extensively off label due to material cost savings compared to the branded drugs. The two leaders, Lucentis and Eylea, are both set to come off patent over the next five years, so there is a proliferation of biosimilar development. The current marketed drugs will likely experience biosimilar competition in 2020.11

Existing DR/DME Treatment: Limited Options

Recently, there have been many advances in ocular imaging, healthcare automation, and a push toward distributed care. For example, Notal Vision has developed an in-home optical coherence tomography (OCT) machine for remote monitoring of retinal disease progression. IDx received approval in 2018 from the U.S. Food and Drug Administration (FDA) for an artificial intelligence algorithm to detect diabetic retinopathy that can be used with any automated retinal imaging system. And telemedicine is seen as a clinically validated and cost-effective means to improve DR screening in a poorly compliant demographic.12 Advances such as these, combined with access to successful therapies like anti-VEGFs, have made improvements in the diagnosis and management of DR and DME. We may expect these developments to continue the downward trend for the incidence of blindness due to DR, in the face of climbing numbers of aged diabetics.13

Still, the treatment options currently are limited and include:

- Anti-VEGF medication. These first-line therapies (as named at left) work by blocking the production of new blood vessels and reducing macular swelling. This slows vision loss and improves vision. These agents are administered via injections into the eye.

Lucentis was the first anti-VEGF approved that demonstrated sustained maintenance of vision improvement. Currently, Eylea is the standard of care and the market-leading drug in virtually all retinal disorders. It has seen particularly rapid growth in the DME market as studies have shown that it may be superior to the alternatives in DME patients with more severe disease.14 Interestingly, the number two retinopathy drug, Avastin, is used off label in ocular indications, but is widely reimbursed.

These three medications vary in costs. As of 2015, Eylea costs $1,850 per 2.0 mg dose, Lucentis costs $1,170 per 0.3 mg dose, and Avastin costs about $60 when repackaged into 1.25 mg syringes (requires a local compounding pharmacy).15 The treatment regimen is different for each of these three products, but patients typically receive three to eight injections per year following initial loading doses to halt active bleeding and reverse edema quickly upon diagnosis. Treatment must continue indefinitely, and there may be a rapid decline in vision when treatment is stopped.

- Steroids. Common corticosteroids—e.g., dexamethasone, fluocinolone acetonide, and triamcinolone acetonide— are low-cost, readily available anti-inflammatory agents that can be administered orally, topically, as injections, or as sustained-release implants to reduce macular swelling. Corticosteroids have many known systemic and ocular side effects, including elevated intraocular pressure and cataract formation, so these are most appropriate for short-term relief of tissue thickening.16

- Laser surgery. Laser photocoagulation can seal leaking blood vessels to reduce retinal swelling. It can also shrink blood vessels and prevent them from regrowing. Laser photocoagulation may halt active bleeding, but the therapy itself causes permanent tissue damage. Thus, this approach remains popular only for non-centerinvolved diabetic retinopathy.

- Vitrectomy. This common surgical procedure to remove the vitreous in the central eye cavity may be employed in the case of vitreous hemorrhage, a common complication of proliferative DR. Removal of the vitreous prevents further fibrovascular growth.

The anti-VEGF drugs represent the newest class of approved treatment options, having been available since 2004 (Macugen®), with Lucentis gaining the first approval for DME in 2012, and later for DR in 2015. The others are more traditional approaches that have been in use for decades.17

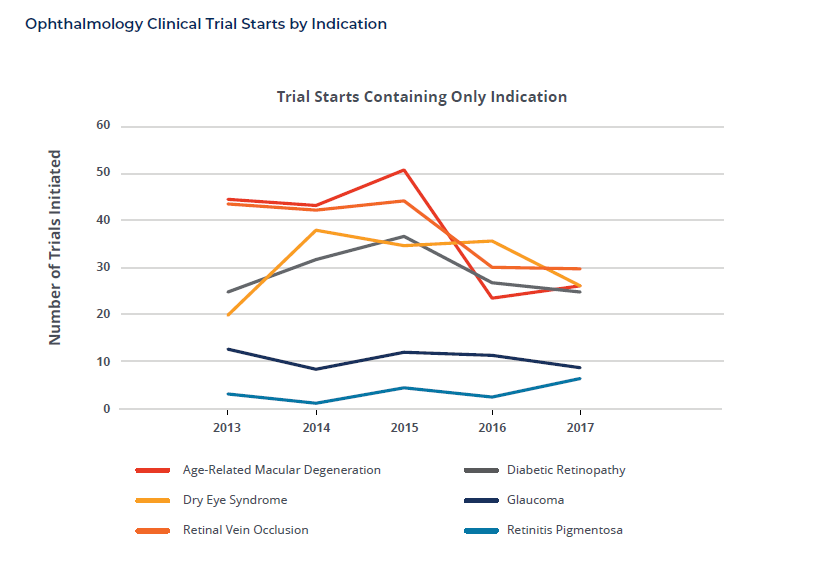

Clinical Research: A Crowded Field

Although the number of DR clinical trial starts has remained relatively flat in recent years, with an overall decline for new trials across all of ophthalmology, drug developers may expect exceedingly high research competition from late 2018-2020. There are many DR and DME compounds in clinical trials with 20 programs or more anticipated to be recruiting Phase II and Phase III patients during this period. This includes five studies starting in the second half of 2018 for Momenta/Mylan, Novartis, and Roche alone that will recruit over 3,000 patients.

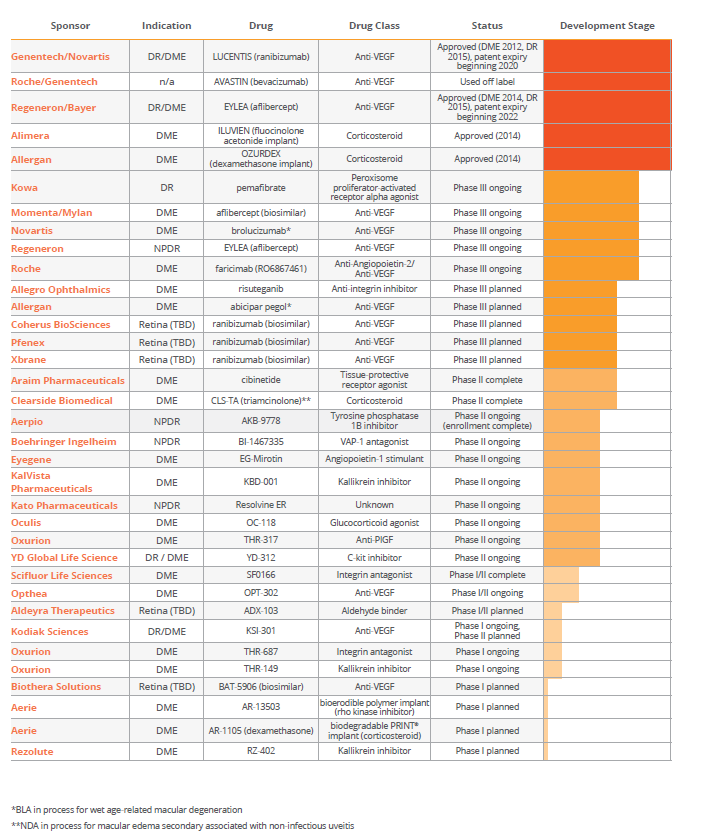

Across retinal disease areas, research is aimed at finding new mechanisms of action, combination therapies, and more convenient, long-acting therapies designed to improve compliance, which is poor in most patient populations.18 For DR and DME, researchers are pursuing novel pathways as well as new anti-VEGFs, including biosimilars. And in addition to the already approved therapies, we may expect several others coming across retinal diseases—brolucizumab from Novartis, abicipar pegol from Allergan, CLS-TA from Clearside, and Yutiq™ from EyePoint—which will impact the standard of care and research environments over the coming years.

Status of Ongoing Diabetic Retinopathy Programs (as of September 2018)

Investigator Viewpoints

In order to better understand current expert thinking on how diabetic retinopathy patients are treated, Syneos Health prepared and distributed an electronic survey to solicit feedback from retina-specialist physicians in 32 countries across North and South America, all parts of Europe, Asia-Pacific, including Australia and New Zealand, as well as Africa and the Middle East. Several questions were posed to assess current practices in both the routine care and clinical trial settings for patients with proliferative and non-proliferative diabetic retinopathy and diabetic macular edema. Investigators were asked to address pertinent questions and preferences for access to and use of anti-VEGF and other therapies, as well as continuing interests for research-stage therapies. All 203 global responses were returned in July 2018 and evaluated by Syneos Health medical and drug development experts during August and September 2018 in order to compile this report. Responses have been incorporated from the following countries:

From this, we are able to gain valuable insights about current preferences and practices, including important regional differences that may influence study design and operational planning for forthcoming clinical trials.

DR/DME Treatment Preferences

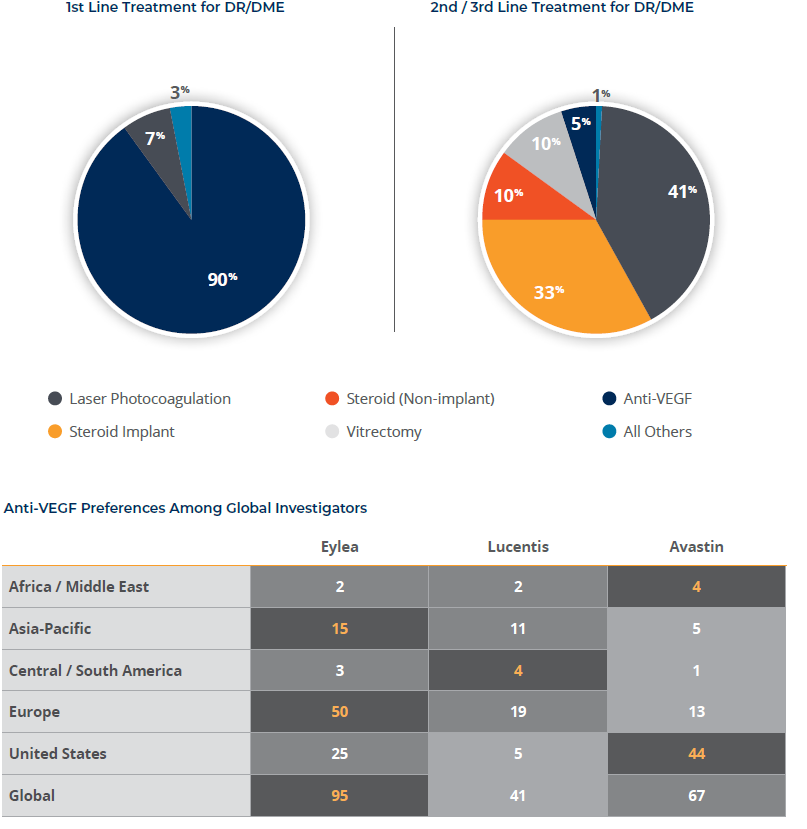

Perhaps not surprisingly, anti-VEGF agents are well established globally as first-line treatment for DR/DME and are used first nine out of ten times globally. Laser photocoagulation comes in a distant second as a first-line therapy (7 percent), used first only outside of North America. With a small number of respondents, it is worth noting the exception in Central and South America where laser photocoagulation is still a dominant first-line treatment, used over one-third of the time. This is largely explained by the low 13 percent reported reimbursement rate for costly VEGF inhibitors in this region.

There is strong correlation between second- and third-line treatment choices, so they have been grouped for this report. In general, when anti-VEGF therapies are not used because they are either not approved or not reimbursed, physicians turn to historically traditional disease management techniques such as laser photocoagulation, steroids and vitrectomy as their fallback. Laser photocoagulation is most common (41 percent) followed by steroid implants like Iluvien and Ozurdex used one-third of the time. There are also some regional variances in this group. For example, vitrectomy is performed almost exclusively in Central and South America (25 percent of the time), perhaps in part due to lower access to steroid implants (25 percent), which are selected half as often as in other locations. Also, non-implanted steroids are rarely chosen in Europe and Africa/Middle East, listed by only five investigators across both regions.

There is no clear consensus among regions about which VEGF inhibitor is preferred, though Eylea comes in the most preferred overall across all global respondents. The choice appears to depend largely upon drug availability and reimbursement status. Preferences in the two largest response groups are highly divergent; Eylea is heavily preferred in Europe, selected first by 61 percent of investigators; whereas Avastin is preferred by more than half (59 percent) of U.S. investigators, despite that its use in DR/DMR is off label.

Note: The orange number is the most selected as first preferred in each region. The three shades of gray represent the standardized weighted average of responses for first choice (4 points), second choice (2 points), and third choice (1 point) in order of preference for each drug.

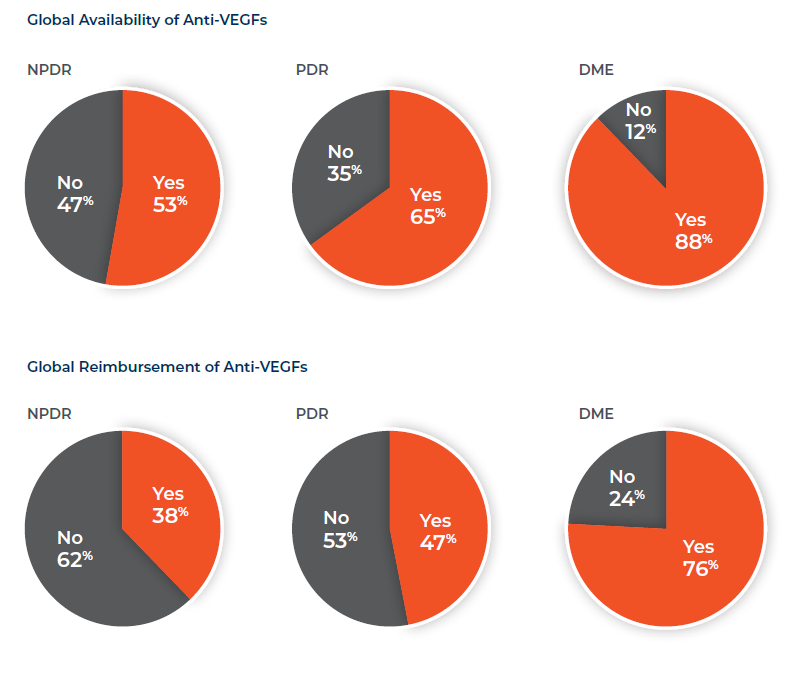

Availability and Reimbursement of Anti-VEGF Therapies

Anti-VEGF drugs are widely approved and marketed around the world for the treatment of all forms of diabetic retinopathy. This is the case even for Avastin despite it not being developed for eye diseases. DME has the highest rate of approval, but anti-VEGFs are increasingly available across broader diabetic retinopathies with some of those approvals coming in later years. Europe trails all other regions for VEGF inhibitor availability in PDR and NPDR.

Payers reimburse for anti-VEGFs in most regions of the world, although coverage is lagging in APAC (13 to 45 percent) and Central / South America (12 to 69 percent) for each disease. Reimbursement is also comparatively low for PDR and NPDR in Europe, linked with the previously-indicated low availability. With its earliest approvals, Lucentis has the highest reimbursement rates globally and for all DR varieties, above 95 percent in the United States. Despite its wide acceptance, Avastin reimbursement is strong only in the U.S. and Africa /Middle East.

Treatment Practices for Diabetic Retinopathies

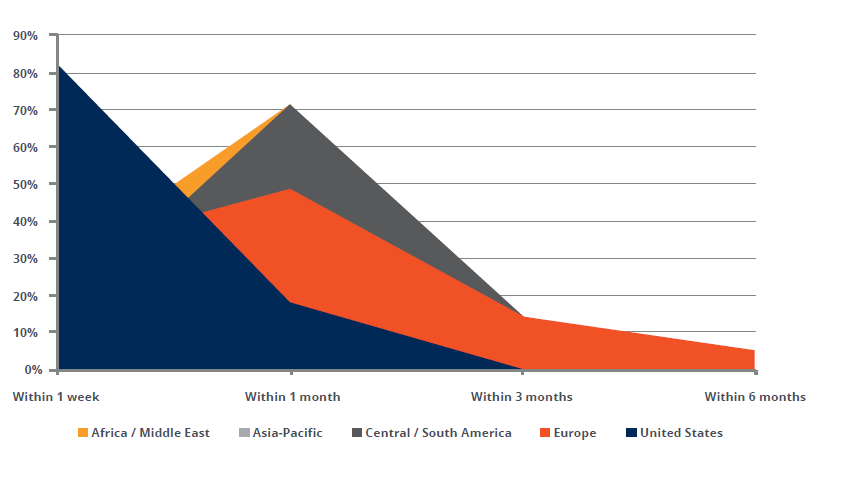

We know that improved detection of DR, and thus earlier intervention, can lead to better health outcomes.19 DME, in particular, is treated quickly after diagnosis—almost always within a week in the U.S. and for half of the cases in Asia-Pacific—and within one month for 91 percent of respondents globally. The time to treat trends longer In Africa/Middle East and Central/South America and even in Europe there is more tolerance for “a wait-and-see approach” where 20 percent of cases are first treated between two to six months.

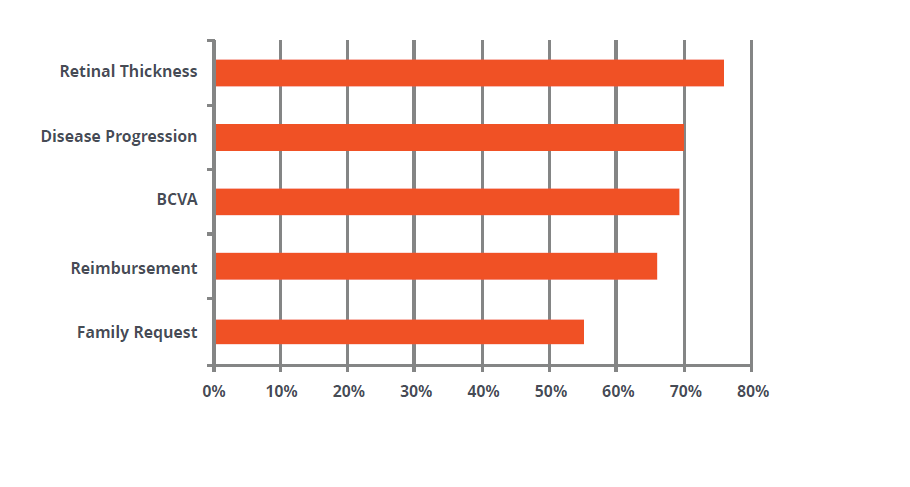

The reasons for choosing one anti-VEGF over another are multifactorial and include retinal thickness, disease progression, best-corrected visual acuity (BCVA), reimbursement, and patient and family influences. On this line of questioning in our survey, respondents indicated:

- Retinal thickness by OCT is pulled to the top of the list in part because it is a determining factor for 86 percent of U.S. respondents. Globally, investigators look for 300+ microns as their trigger point.

- Physicians in Europe are far less likely than their counterparts in other regions to base their decision on disease progression (54 percent) or BCVA (59 percent). Disease progression is most often marked by worsening edema or BCVA. BCVA scores even as good as 20/30 serve to trigger treatment.

- Reimbursement is a choice factor everywhere, but comparatively lower for Europe (54 percent) and Central/South America (50 percent). In both regions, there were more comments regarding country and institutional requirements dictating reimbursement.

- The views of patients and their families are generally not factors for physicians in Europe (32 percent), whereas they are important in other regions.

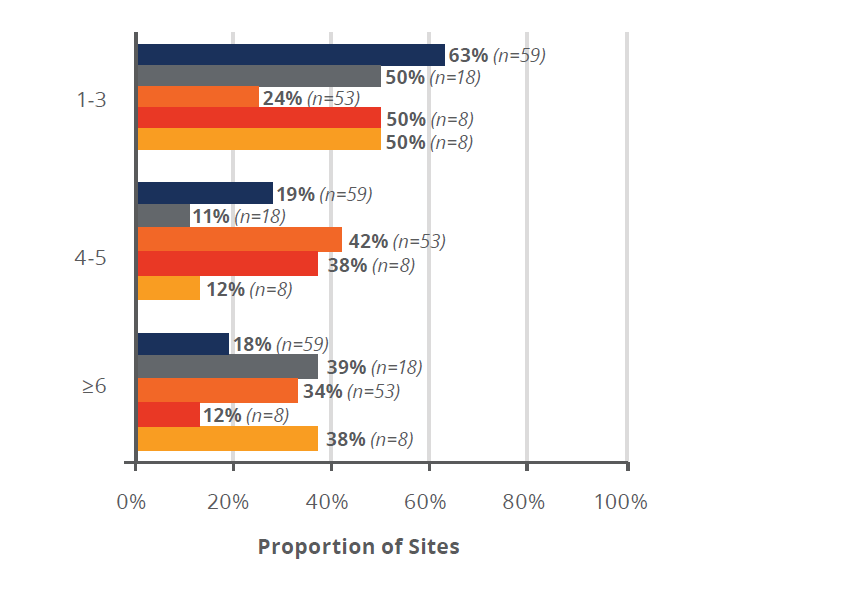

With the exception of Europe, ophthalmologists do not wait long to switch from a low-performing anti- VEGF treatment; at least half of the time, they make the switch after only one to three injections. In Europe, by contrast, physicians wait until after at least four injections to switch treatments three-quarters of the time, and often they wait until after six or more.

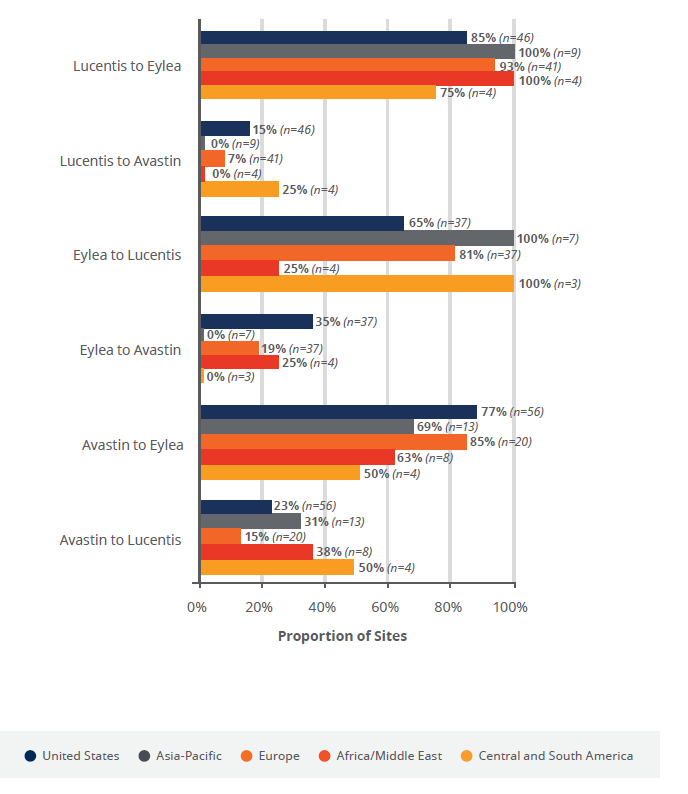

When practitioners see a low response in users treated with Avastin and Lucentis, they overwhelming choose to switch patients to Eylea. When switching from Eylea, physicians switch almost exclusively to Lucentis, except in the U.S. where over a third choose Avastin.

Time to Treat for Newly Diagnosed DME

Factors for Choice of Anti-VEGF

Number of Doses Before Switching

Anti-VEGFs Switching Patterns

Interest in Further R&D

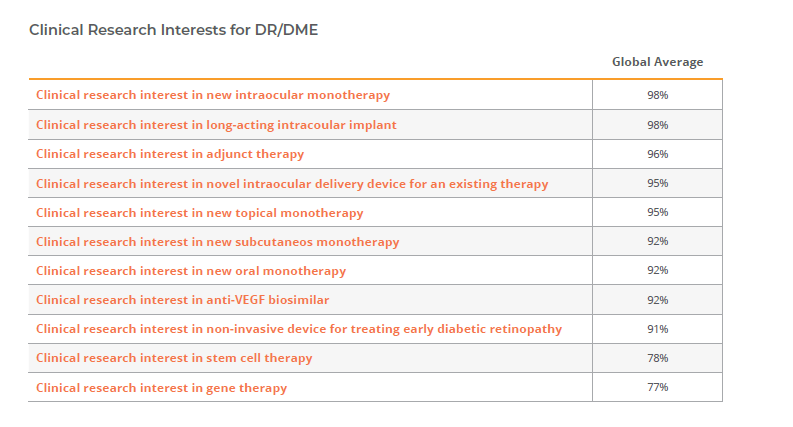

There is broad global interest among investigators in continuing research to develop new drugs for all diabetic retinopathies, by any modality, underscoring the fact that there remains high-unmet need in the market. Investigators are eager to be involved in research for treatments including:

- anti-VEGF biosimilars

- monotherapies by any delivery modality

- intraocular implants of existing and new therapies

- adjunct and co-therapies

Interestingly, while newer technologies such as stem cell and gene therapies are of interest, they are less compelling to respondents than traditional treatments for this disease area. Across regions, the percentage of investigators expressing interest in anti-VEGF biosimilars, for example, ran consistently in the high 90s. However, the percentage who were interested in stem cell therapy or gene therapy dipped as low as 69 percent in the first case and 67 percent in the second. We know from the programs identified in this report and in published papers on the future of DR care, our increasing understanding of disease pathways is taking targets beyond anti-VEGFs to include Angiopoietin-2 inhibitors, Tie2 receptor stimulators, kallikrein inhibitors, integrin antagonists, anti-PlGFs, and others via injection, topical, oral, and subcutaneous delivery, as well as long-term inserts.20

Globally, more than 90 percent of investigators are interested in the majority of research options presented; however, stem cell therapy (global average of 78 percent) and gene therapy (global average of 77 percent) are the research options of lowest appeal. Asia-Pacific physicians had the lowest proportion of interested sites in 7 out of the 11 research options considered.

Upcoming Clinical Trials

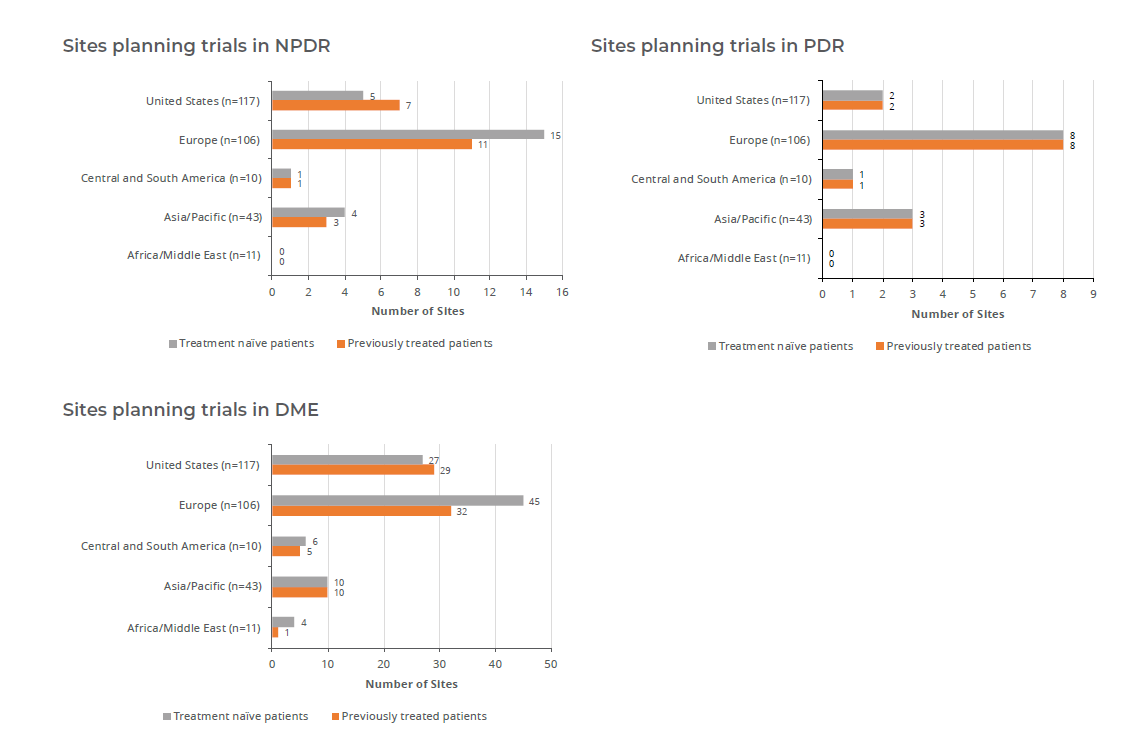

Respondents were asked to quantify the number of trials that they expected in NPDR, PDR, and DME for 2019, and the results confirm that this is an exceedingly competitive area for research on a global scale. This is particularly the case with DME.

A majority of sites around the world are also planning trials in NPDR for 2019, although they amount to far fewer than in DME.

Recent trials have recruited predominantly treatment-naïve patients. Newer studies, however, appear to be seeking to improve outcomes for low- and non-responders by including patients who have been previously treated. In the U.S., for example, the number of planned trials include previously treated patients actually exceeds the number excluding them.

Almost three-quarters (72 percent) of sites in Europe expect to participate in DME trials, as do almost half (48 percent) of the U.S. sites. The fewest DME trials are planned for Africa and the Middle East.

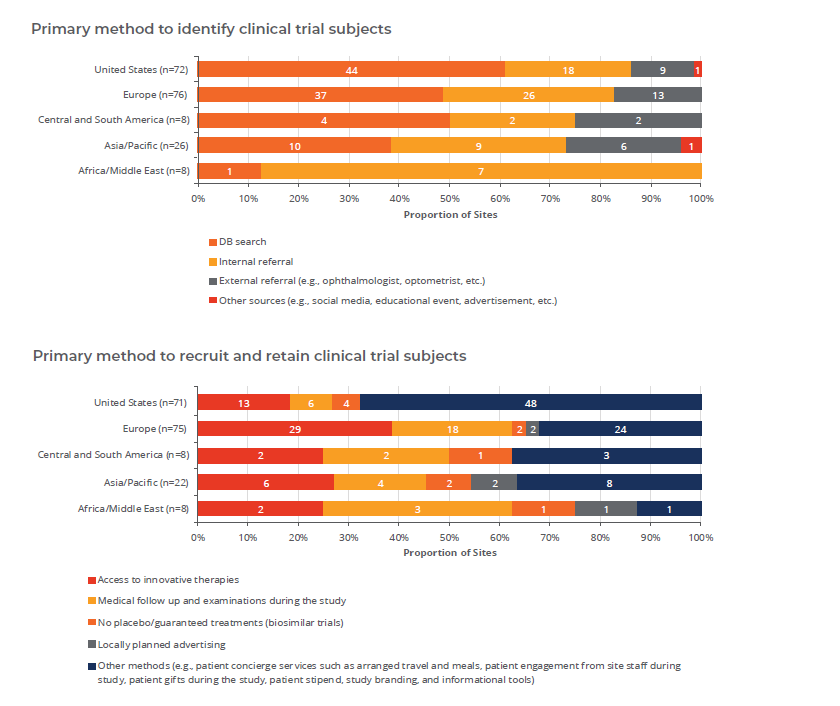

Methods of Patient Recruitment

Sites find clinical research subjects via many means and sources. The most important two across all regions are existing database and internal referrals. In the U.S., optometrists are highly influential in referring trial subjects (named by 19 percent of respondents), but this is not true in any other region.

Because of readily available anti-VEGF therapies and tendencies to treat quickly, external referrals are less successful, and no clinical trial will be able to establish new referral patterns; these are determined by existing site networks and should be evaluated as part of site selection. There is accelerating access to and use of mydriatic and nonmydriatic retinography in even the primary care settings, meaning clinical trial subjects may be pushed to retina clinics from a variety of original sources, and understanding these patterns is critical to trial enrollment.21

Conclusion

Broadly, the confluence of a global aging population and expanding diabetes epidemic have contributed to a rapid incidence growth for diabetic retinopathy. There remains a significant unmet need across the disease spectrum with few options for either proliferative or non-proliferative DR, and moderately successful treatments for DME. DR is a major cause of vision impairment worldwide, and the fastest-growing disease of all critical ophthalmic indications.

Though anti-VEGF therapy has proven a major breakthrough for DR and DME, there are still a third of sufferers with low or no response. Anti-VEGFs are increasingly available on a global scale, but come at significant financial cost and treatment burden. One of the three leading drugs, Avastin (bevacizumab), isn’t even indicated for any ocular disease. Current approved drugs are nearing their patient cliff, which has created a very attractive commercial and clinical opportunity supporting new drug development. In fact, we can expect that competition from biosimilars will spur further development of novel treatments. The commercial landscape is going to shift dramatically in the early 2020s with both biosimilars and new innovative drugs coming to market.

For those who do venture into this arena, the retina clinical development space will remain highly competitive over the next several years with dozens of new therapies progressing to late-stage development. Researchers are developing a better understanding of the types of treatments that are needed beyond the first-line therapies available today. Thus, there are major opportunities for biosimilars, novel biochemical pathways, and improved treatment regimens and delivery techniques aimed at providing more options and easing patient burden. Successful combination and adjunct therapies have proved elusive so far, but there have been major improvements in diagnostic and disease monitoring technologies, meaning patients are getting diagnosed earlier in their disease course.

Newer trials increasingly seek low- and non-responders for existing therapy, and it is exceedingly difficult to recruit the populations that meet such protocol definitions while avoiding those patients who are simply undertreated or poorly compliant. As treatment options outside of clinical trials become more widely available, it may become even more difficult to find patients interested in participating in research.

Though the focus here has been on diabetic disease, there will be many major age-related macular degeneration (AMD) studies running over this same period, which will mean high competition for finite site resources across the retina spectrum. Sponsors need to understand these realities in order to apply past lessons, deliberately manage risk, and carefully plan to be successful in this space during the next half decade.

References

1. https://nei.nih.gov/eyedata/diabetic

2. “The High Cost of Low Vision: The Evidence on Ageing and the Loss of Sight,” The International Federation on Ageing. Accessed at: http://www.ifa-fiv.org/wp-content/uploads/2013/02/The-High-Cost-of-Low-Vision-The-Evidence-on-Ageing-and-the-Loss-of-Sight.pdf

3. https://www.tmcnet.com/usubmit/2010/04/16/4732193.htm

4. www.un.org

5. www.cdc.gov/diabetes/statistics

6. https://www.visionweb.com/content/consumers/dev_consumerarticles.jsp?RID=16

7. Lee R, Wong TY, Sabanayagam C, “Epidemiology of diabetic retinopathy, diabetic macular edema and related vision loss,” Eye Vis (Lond) 2015; 2: 17. Published online 2015 Sep 30. doi: 10.1186/s40662-015-0026-2

8. Cheung N, Mitchell P, Wong TY. Diabetic retinopathy. Lancet. 2010;376(9735):124–36. doi: 10.1016/S0140-6736(09)62124-3.

9. https://nei.nih.gov/health/macular-edema/fact_sheet

10. Datamonitor Healthcare: Retinal Disorder Forecast, October 13, 2017.

11. Datamonitor Healthcare: Retinal Disorder Forecast, October 13, 2017.

12. Tozer K, et al, “Telemedicine and Diabetic Retinopathy: Review of Published Screening Program,” J Endocrinal Diabetes, 2015; 2 (4)

13. Sabanayagam C, et al, “Ten Emerging Trends in the Epidemiology of Diabetic Retinopathy,” Ophthalmic Epidemiology 2016, VOL. 23, No. 4, 209-222.

14. Cowen Equity Research, “Ophthalmology: A Focus on Advancing the Standard of Care,” Therapeutic Categories Outlook, March 2018

15. Ross EL, Hutton DW, Stein JD, et al; Diabetic Retinopathy Clinical Research Network. Cost-effectiveness of aflibercept, bevacizumab and ranibizumab for diabetic macular edema treatment: analysis from the Diabetic Retinopathy Clinical Research Network

Comparative Effectiveness Trial. JAMA Ophthalmol. 2016;134(8):888-896

16. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5468529/

17. https://www.accessdata.fda.gov/scripts/cder/daf/

18. Cowen Equity Research, “Ophthalmology: A Focus on Advancing the Standard of Care,” Therapeutic Categories Outlook, March 2018.

19. Liew G, Michaelides M, Bunce C. A comparison of the causes of blindness certifications in England and Wales in working age adults (16-64 years), 1999-2000 with 2009-2010. BMJ Open 2014; 4(2): e004015

20. Stewart, MW, “Future Treatments of Diabetic Retinopathy: Pharmacotherapeutic Products Under Development,” EMJ, October, 2017.

21. Corcóstegui B, et al, “Update on Diagnosis and Treatment of Diabetic Retinopathy: A Consensus Guideline of the Working Group of Ocular Health (Spanish Society of Diabetes and Spanish Vitreous and Retina Society,”) J Ophthalmol, Volume 2017, Article ID 8234186.